Editor: Emanuele Marabella

“Palantir is an AI imposter engaging in spurious games to inflate its books and obfuscate its less sexy role as an overhyped data consultant.” - The Bear Cave

This is how The Bear Cave, one of the most prominent Substack publications focused on companies’ misconduct with over 48k subscribers, described Palantir.

However, these allegations are not only misleading but denote a severe lack of understanding of the company.

In this article, I’ll show why the key arguments raised in the report lack substance and look more at an attempt to capitalize on the rise of interest in Palantir rather than providing an accurate analysis.

Hi, I’m Arny. Thank you for joining 2.091 investors who receive the deepest Palantir research. Please hit the ❤️ button if you enjoy today’s article.

“Palantir is a black box”

This argument became popular due to Jim Cramer's comments at Palantir DPO.

“I think it's too much of a black box to get a real read on the business so be careful” - Jim Cramer

While the assertion seemed plausible back then due to the relatively little and mediocre information available, almost three years later, there are no excuses:

Palantir hosted several demos, which can be found on YouTube;

Palantir released a wide Foundry documentation on its website;

Palantir allows everyone to get a base-level Foundry certification for free.

With the current information available, even people like me that don’t use the platform can understand what Palantir is and how the software is actually used.

In other words, laziness is the only excuse to ignorance.

Interestingly, despite seeing Palantir as a “black box where the process of seeking information might leave one with more questions than answers” the Bear Cave author is confident in expressing that Palantir is an “AI imposter.”

“Palantir is an AI imposter”

According to the report Palantir is misleading investors by seeing itself as an “AI leader.”

The most prominent IT research providers back this leadership position:

Forrester;

Gartner;

IDC.

Therefore, affirming that Palantir is an “AI imposter” implies that all the research providers mentioned are impostors as well as they would fail in performing their core operations.

Unfortunately, the Bear Cave doesn’t provide evidence that invalidates the judgment of the mentioned IT research providers.

Furthermore, the report was published on the exact day of AIPCon, where some of the key Palantir clients showcased their results and satisfaction by using Palantir’s AI platforms.

In the picture below, you can see key representatives of Panasonic Energy, HCA Healthcare, and Cleveland Clinic sharing their satisfaction with the Palantir platform.

If Palantir was an AI impostor, these companies and executives would be impostors as well for promoting results that are not true.

If everyone is lying about Palantir’s capabilities the US would be at serious risk by making it run with crucial federal agencies like:

the National Nuclear Security Administration;

the Army;

the Centers for Disease Control and Prevention.

If Palantir were an “AI impostor,” we would accept that all the institutions above are also impostors for failing to detect Palantir’s fraud.

Edwin Dorsey, the author of the report, is surely a brilliant writer. However, his background doesn’t seem adequate to properly assess Palantir’s AI capabilities.

“Palantir is a consultancy”

The Bear Cave reports that while Palantir presents itself as an AI leader, it is just a “glorified consultancy company.”

Palantir does have a consultancy component in its business when they initially solve a customer problem. Palantir’s Forward Deployed Engineers collaborate in strict relationships with customers like McKinsey or BCG consultants do. However, differently from the companies mentioned, Palantir’s FDEs don’t only “consult,” they use Palantir platforms to actually solve a client’s need so that the customer becomes a regular user of the platform, which is the core offering.

What is defined as criticism, in reality, is a key differentiator for Palantir as discussed in the previous article:

“Thanks to their proximity to problems, FDEs generate crucial insights that are not only critical to help solve similar problems but also develop new features in Palantir which can subsequently be used to empower FDEs and clients.” - Palantir Bullets

The result is that saying “Palantir is a consultancy” is as wrong as saying “Apple is hardware.”

A simple effective way to deny this allegation is by comparing Palantir’s ~80% Gross Margin with that of reference B2B Software companies that also have a minor component of consultancy in their business:

ServiceNow: 79%;

Salesforce: 74%;

Snowflake: 66%.

Consultancy companies have much lower Gross Margins:

Accenture: 32%;

Leidos: 13%.

Jacobs Solutions: 21%.

If Palantir were mainly a consultancy company it would not have ~80% Gross Margin similar to ServiceNow where only 3-5% of the Revenue is generated from Consultancy. If Palantir offered a misleading allocation of costs then that would be an accounting irregularity.

The Bear Cave report does not provide evidence of accounting irregularity regarding the method Palantir reports its costs.

“Palantir inflates its financial numbers”

Palantir is accused of inflating its financial metrics by making investments in companies and requiring those companies to buy Palantir products.

The criticism is related to SPACs, which we have been widely discussing for one year here at Palantir Bullets. While the criticism is legitimate, the assertion is misleading.

Palantir paid ~$400mn in overall SPACs investments and received commitments for ~$700mn of Revenue for the usage of Palantir Foundry over the contract length.

The move was surely unusual in the corporate context, but the report does not provide evidence of an eventual illegality. Palantir invested in the companies at the same market conditions while also having a commercial agreement for the usage of the platform.

As seen in the latest results, even if Palantir sold the shares of most of the SPACs, these companies that are not bankrupt are still clients. This proves that the investment agreement and commercial agreements were separate as Palantir reported in a reply to the SEC Division of Corporate Finance.

While it is true that SPACs generated a Revenue boost, declaring that Palantir “inflates” creates the deception that this is the normal way the company operates. As a matter of fact, Palantir has been growing its Commercial Revenue and customer count by ~22% and ~62%, respectively, in Q1 excluding SPACs.

Furthermore, Palantir assumed both the risk of losing capital and the commercial risk from companies in a relatively weak condition. A risk that manifested itself creating not only losses in terms of capital but also the loss of the commercial contracts from the companies that failed.

Accounting irregularities

The Bear Cave hints at accounting irregularities from a sentence in the 10-k, which was called a “critical audit matter” by the author:

“Management applies significant judgment in identifying and evaluating any non-standard terms and conditions in customer arrangements which may impact the determination of performance obligations or the timing of revenue recognition.” - Ernst & Young, Palantir’s auditor, Palantir 23Q1 10-k.

What’s defined as a “Critical audit matter” of the last 10-K is just a regular text written since the 20Q4 10-k, which was already present before the first SPAC investment was performed.

Very similar wording can be found on Salesforce’s 10k. I am not a CPA, but I don’t see evidence of irregularities, only a warning where potential problems could arise.

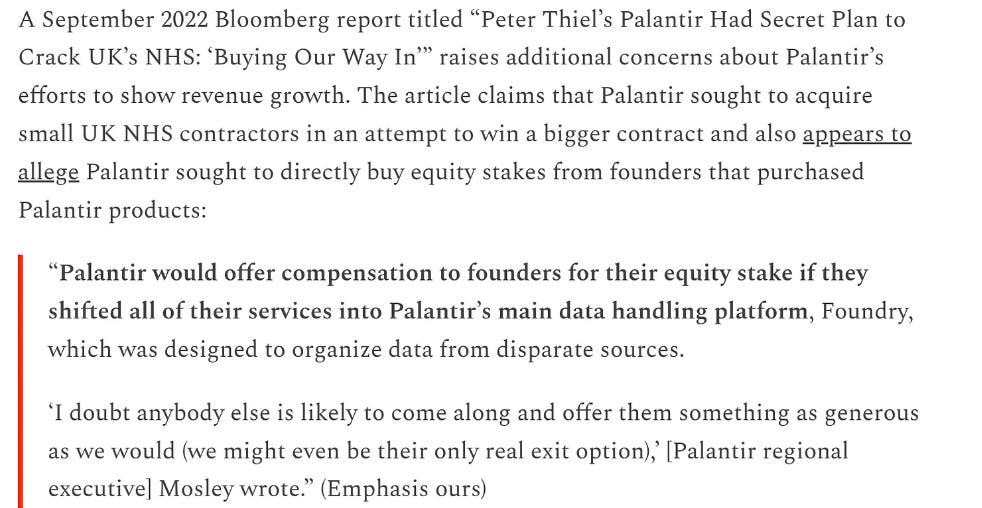

“Palantir buys its way in”

The report eludes to hints of misconduct as Palantir attempted to buy their way into the UK NHS by attempting to purchase equity stakes from founders who supply the UK NHS.

If this is illegal, it would be helpful to be shown some evidence, however, no evidence of illegality was provided in the report.

“Palantir sales management is straight up mentally ill”

A further point raised is related to the complaints of salespeople on Glassdoor.

Negative comments from salespeople are not enjoyable but not surprising given that Palantir has been very “engineering” focused and reluctant to hire salespeople.

Furthermore, underscoring the salespeople without considering what the clients say about the product, which is not a mere consultancy project, misses the full picture.

Product reviews on Gartner rank Palantir among the best products. Therefore, I see the critics on Glassdoor as just a negative, solvable data point that doesn’t affect the real Palantir thesis.

Executive resignation

The resignation of Jeff Buckley as Chief Accounting Officer is underscored as a sign of Revenue stress.

“Palantir’s Chief Accounting Officer, Jeffrey Buckley, resigned from his role one day after the 10-K was filed. Mr. Buckley served as Chief Accounting Officer for about two and a half years.” - The Bear Cave

While an executive leaving is not a positive sign, it is not necessarily negative. Contextually with Jeff's departure, Shyam Sankar was nominated to CTO from COO. This could be a sign that the management recognized the mistake with SPACs and decided to move on.

Valuation

Given the considerations above, Bear Cave suggests that Palantir should trade at a low revenue multiple in line with a consultancy company, rather than the current ~13x EV/Sales. In the previous article, I showed how Palantir's financial numbers are, differently from a consultancy business, very scalable thanks to the software component.

Saying Palantir should be valued as a consultancy company is the equivalent of saying Apple should be valued as HP (HPQ) because they are a hardware company.

While it is true that Apple mainly sells hardware, ignoring that most of the value comes from a sublime combination of hardware and proprietary software would be a failed representation of reality.

While it is impossible to predict how the stock will move, the validity of the accusations will emerge over time.

Conclusion

The Bear Cave report lacks understanding of the business and its assertions seem to be a vain attempt to capitalize on the relative popularity of Palantir after its +130% YTD performance.

I leave space for discussion about whether leveraging an audience of almost 50k with false claims should require further scrutiny.

I frankly hope short sellers will at least put some effort into future reports.

“The Bear Cave is a bear cave. They can stay in their bear cave.” - Alex Karp

Yours,

Arny

Good article! We need some better short reports!

You have not provided any evidence of Palantir AI product or solution... in fact on Palantir AIP event they didn't show their AI either.

I am still looking for Palantir AI demonstration.. I can't find anywhere!!! this is alarming.