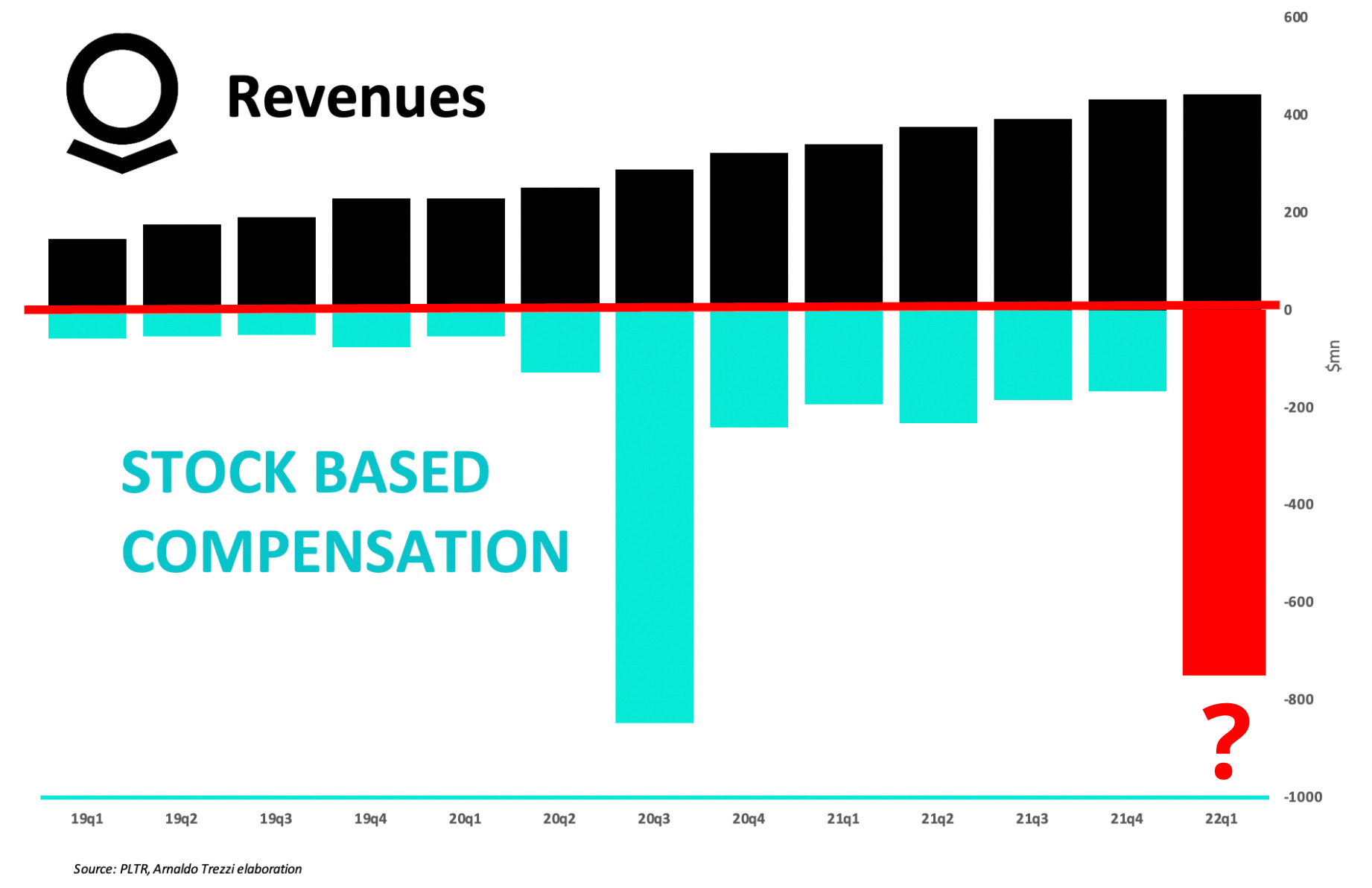

When will Palantir SBC ease?

Some say SBC does not matter, others say SBC makes Palantir an “unprofitable trash”. So what’s the reality, and even more important, what’s the real cost of SBC?

This article has first been published on Darntons (@DartonsMedia).

Among the controversial arguments related to Palantir ( PLTR 0.00%↑ ), StBased-Compensation (“SBC”) is one which creates discussion. Some say SBC does not matter, others say SBC makes Palantir an “unprofitable trash”. So what’s the reality, and even more important, what’s the real cost of SBC?

SBC is a non-cash expense. Who bears the cost?

Stock-Based-Compensation is a form of compensation for employees in addition to salaries. While salary is in cash, SBC is mainly issued in the form of Restricted Stock Units (“RSU”) or Stock Options. Therefore, SBC does not involve any cash expense for the business, in the financial jargon is a “non-cash expenditure”. Nothing is free, so someone has to bear the cost.

More in detail, SBC mainly assumes two forms:

Restricted Stock Units (“RSU”): employees are given newly issued shares as they work for the company. However, employees will be able to effectively receive them when the vesting period ends. RSUs are generally vested in 3-5 years.

Stock Options: employees are given the financial option to acquire shares of the company at a predetermined strike price until a predetermined maturity. These are typically vested in 8 years. These options have considerable value only if the price is above the exercise price, “strike price”. A cash inflow is generated for the company when the employee exercises these options.

With these forms of compensation, the company incentivizes talents to stay long and deliver the best results since the value they receive is dependent on the business performance and in turn market performance.

SBCs are granted when employees are hired or at renewal after the vesting period.

At the end of the vesting period, the employee finally has access to the RSU and the Options he deserved. After these RSU and Options are vested, the employee has full ownership and the company does not need to recognize further expenses on those. If an employee leaves the company, the related RSU or Options will not be vested and therefore cancelled.

In terms of accounting, during the vesting period, the company recognizes as SBC the relative expenses of the RSU and Options that are vesting.

The amount of SBC is determined at the moment of the grant date. After the grant date changes in price do not affect the SBC recognition of the existing RSU and Option.

Changes in market prices, however, change the number of shares needed to be issued to offer the same package. This could trigger a vicious circle (more on that later!).

Let’s imagine I join Palantir as a software engineer, I will receive $100k RSU per year with a vesting period of 4 years. Yes, $100k is high because to attract me Palantir needs to offer me a comparable offer to Google or Microsoft.

Palantir each year will recognize $100k SBC expense, regardless of the price movements of the stock. Only the price at the grant date matters.

After 4 years, the RSU are vested and I will receive the stocks, now I can sell them or keep them. Palantir now will stop accounting for the related SBC expenses until a new grant.

As a result of my RSUs, the number of Palantir shares will increase, but the company will not incur cash expenses in addition to my salary. However, my additional shares will create a dilutive effect on other shares.

Dilution is this reduction in the % ownership of the company to remaining shareholders.

The implication of SBC – Company vs investor

This kind of compensation, which assumes a meaningful impact on the financials of tech companies, has profound implications for the company and investors.

The company uses SBC as a form of compensation to attract and keep the best talents. Remember, in tech, the top 1% of talent can deliver more results than the remaining 99% combined. SBC creates the incentive for talents not only to stay in the company but to perform at their best creating value for the company. Companies in the early stages love SBC because is a way to stimulate growth preserving cash which could be used for growth, like Marketing & Sales expenditure.

Want the best business performance? You need to hire the very best talents and retain them.

This alignment of interest also benefits investors. However, investors do not fully benefit from future growth as a result of dilution.

Eg. Palantir’s Operating Income adj in Q4 was $124mn, corresponding to +7% QoQ from $116mn. If the number of shares didn’t change, investors would benefit from the full Operating growth per share.

However, due to the +2.4% increase in the number of shares the Operating Income Adj per share is up only +4.4%. The divergence between +7% and +4.4% is due to dilution.

Palantir could have instead paid $167mn in cash to employees, but that would have destroyed the Operating Income, which on a capital-light company like Palantir is a proxy of Free Cash Flow. Having FCF for a company at an early stage as Palantir means that now it can use that cash to further boost its growth.

If instead paid all cash it would need debt its ability to grow would be contained.

We can say that the company diluted 2% in the quarter, 12% compared with last year because investors outside the company have the % ownership of the company reduced.

The risk for investors, therefore, is companies not growing enough to offset the negative effect of dilution.

If the company grows 30% and each year the number of shares grows 30% at the end of the year the company has grown but the intrinsic value of each share has not changed since it would entitle investors to the same FCF per share.

If growth and FCF generation are not strong enough to offset the diluting effects, damages for investors could be disastrous.

When we invest in a business with a strong SBC like Palantir we are not only investing in the business to produce cash but also in the ability of the management to keep investing in the right people to boost growth.

There could be a vicious circle that is very dangerous. If the stock price stays too low and the company needs to provide huge packages the same amount of $ compensation will generate more new shares issued, therefore more dilution!

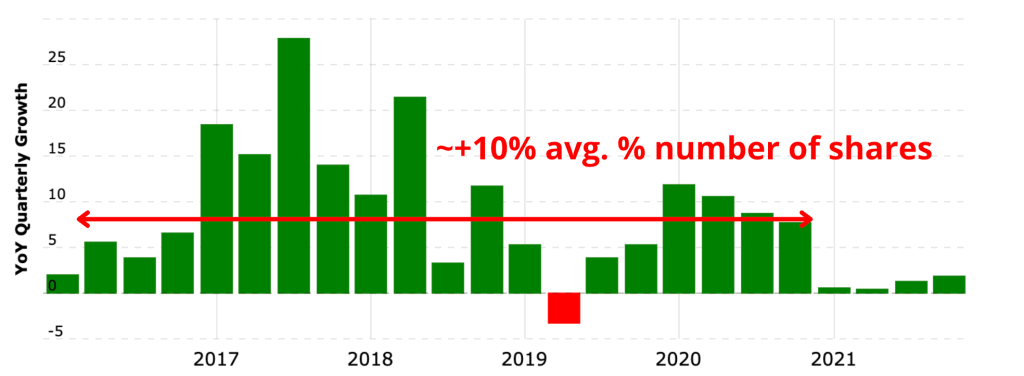

When will dilution ease?

Dilution is a natural process for all companies. In tech since competition for top talents is ferocious and each top talent can deliver very asymmetrical returns companies tend to issue more shares compared with other industries.

Even very mature companies like Google ($GOOG) keep increasing the number of shares by ~3%. However, mature companies typically offset dilution by buy-backing shares.

Palantir currently dilutes at 10%. Karp said there will be a “normalization process” in the next 2 years which makes me think that the dilution will be more in the 5-7% range in line with companies in the expansion phase like AMD ($AMD) or ServiceNow ($NOW) (Palantir competitor?). With the company growing 30%+ that would mean that the intrinsic value of our share grows at least 25%.

Given the importance of SBC for shareholders’ returns, it will be relevant to see in the Q1 results (Q1 outlook) the Remaining Deal Value growing more than Unrecognized SBC, which could be a good sign toward dilution normalization.

Looking at Unrecognized SBC is the most precious clue to understanding the coming SBC.

Unrecognized SBC is the component that the company is committed to providing but which will be recognised as employees performing their job during the vesting period.

Palantir currently has ~$1,8bn Unrecognized SBC. This is composed of $922mn RSU with an avg. vesting period of 3 years and $888mn Options with an avg. vesting period of 8 years.

Therefore, we could expect RSU recognition should generate more than $300nm per quarter (922/12), and Options recognition to generate more than $100mn SBC per quarter (300/3).

As a result, given the current Unrecognized SBC, we should expect at least ~$100mn per quarter, ~$420mn per year. I say “the least” because as we go through the year new grant occur both from existing employees and new employees since Palantir is hiring fast (Q1 Outlook).

In other words, I expect Stock-Based Compensation to be still high for a long time, but what investors should be focused on is that growth should be strong enough to make the impact of SBC less relevant compared with Revenues.

Karp explicitly said that he will pursue GAAP profitability. This combined with the SBC normalization process, makes me think that SBC should gradually decrease from 50% of Revenues in FY21 to ~30% by 2025, corresponding to a 6% dilution compared to 12% as of FY21. If these assumptions hold, we would see Palantir becoming GAAP profitable by 2024-25.

Invest in the leader

Some say business is more important than leaders. That could be true in businesses that don’t change much.

In tech, things move so quickly that leadership matters more than business structure. When we invest in a company like Palantir distributing a considerable number of shares to employees, we are investing in Karp’s and management’s ability to choose the best talent to deliver asymmetrical returns.

SBC is here to stay, but if these asymmetrical returns arrive investors will be better off.

Do you trust Karp’s ability in selecting the most talented people? I do.

Join me on Twitter: @arny_trezzi

View expresses are my own. Do not represent Financial Advice.

I own PLTR stocks.