Palantir's FCF Has a Long Way Ahead

Palantir vs. the best B2B SaaS at $2bn run rate

Editor: Emanuele Marabella

Hi, I’m Arny. If you are new, you can subscribe to spot Palantir asymmetries along with 1.200 investors. Please hit the ❤️ button if you like today’s article.

Paid subscribers also receive weekly in-depth research on Palantir’s financials and strategy. Do you have questions arising from my research? Please book a 1-on-1 meeting.

Meetings with Arny Trezzi

In the previous article (Palantir’s Money Machine Needs Scale) we underlined that PLTR 0.00%↑ ’s Gross Margins provide crucial hints about its FCF potential.

If Palantir can keep scaling while preserving its Gross Margins, that would inevitably unlock GAAP profitability as the operating leverage kicks in.

But how does Palantir compare with its peers? How different is Palantir from the most successful B2B SaaS when they were at the size Palantir currently is?

Palantir vs. Servicenow vs. Salesforce

Palantir’s Gross Profit is currently in line with that of ServiceNow NOW 0.00%↑ and well superior to that of Salesforce CRM 0.00%↑ .

As a reminder, size for software companies is a favorable condition for margins.

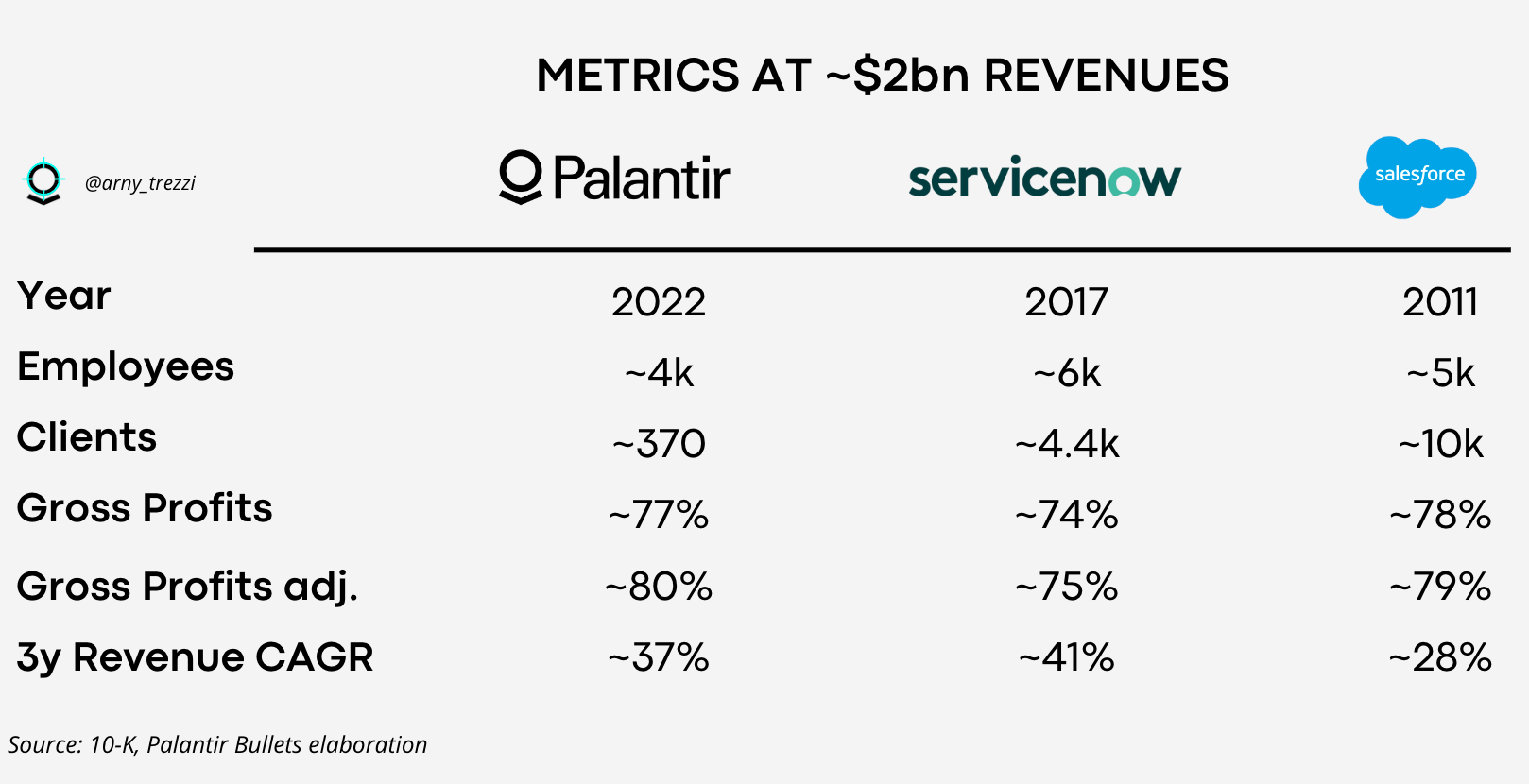

Palantir, at ~77% GAAP Gross Profit, currently shows similar margins to those of ServiceNow, ~3.5x Palantir, in terms of Revenues, and much better than Salesforce, ~15x Palantir, in terms of Revenues.

Salesforce GAAP Gross Margins decreased over time as a result of competition and its aggressive M&A activity, which brought relatively more costs than Revenues.

As we mentioned in the previous article, GAAP Gross Margin includes SBC related to the Cost of Revenues.

By excluding SBC from the Cost of Revenues we can better visualize the FCF potential.

Let’s also add where Servicenow and Salesforce Gross Margins were at with ~$2bn Revenue, which is Palantir’s current run rate.

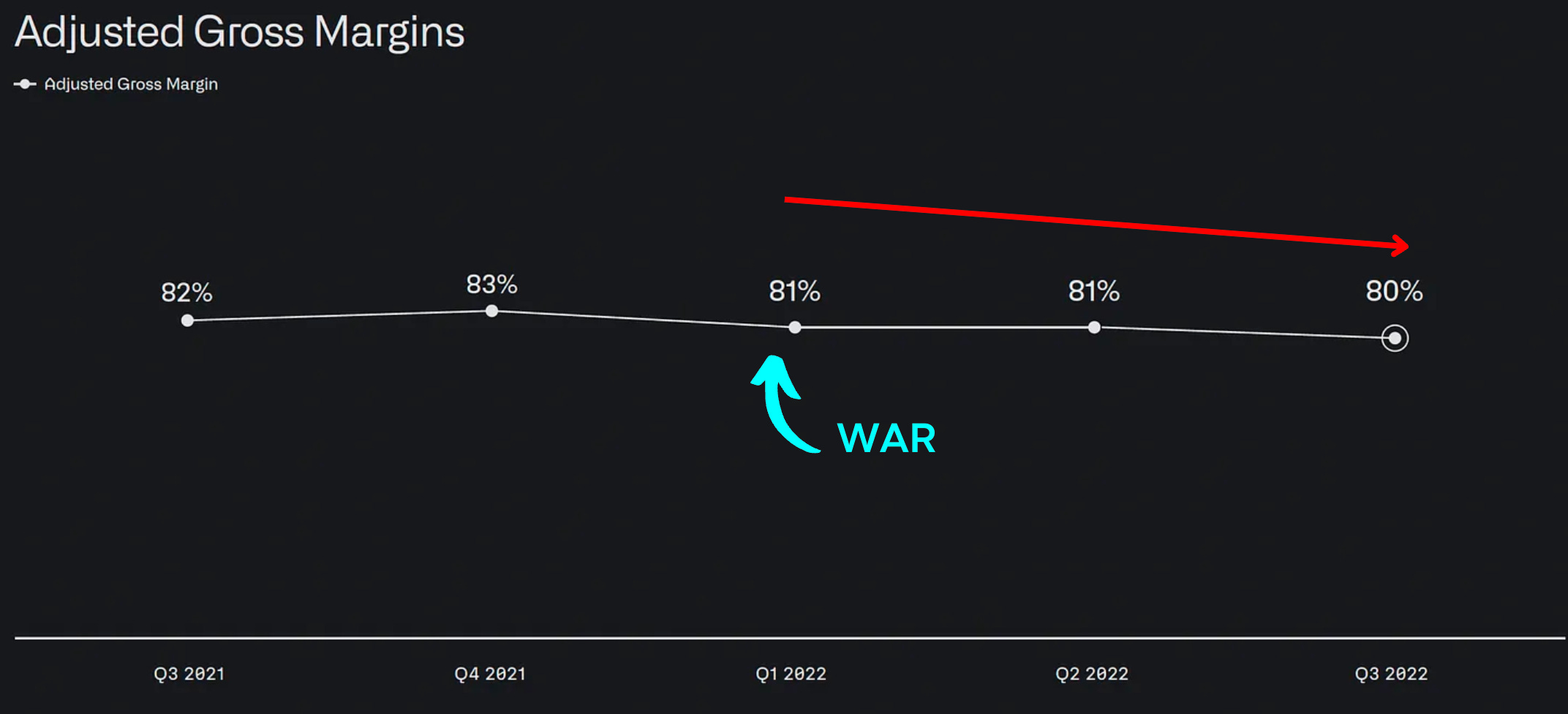

Consider that Palantir’s Gross Margin is currently under pressure. Palantir is expanding aggressively and providing its solutions, according to Karp, to Ukraine for free, which simply means for the moment costs without revenues.

Comparison at $2bn Milestone

We can obtain a meaningful comparison between Palantir, Servicenow, and Salesforce:

Palantir is set to achieve ~$2bn in Revenues with ~370 clients, 10% of ServiceNow’s clients, and ~35% of Salesforce clients.

This is a precious hint that Palantir has a long but prosperous path ahead.

FoundryCon just showed how small-cap companies like Integrity can leverage Foundry. I expect 2023-2025 to be the years of real expansion in the number of clients.

Notably, Palantir needed ~20/30% fewer employees than its peers to achieve ~$2bn Revenue. I consider this an additional sign that despite Palantir's talents being costly ( When will Palantir’s SBC ease?) they are capable of delivering superior results.

22Q3 Peers Comparison

For the sake of completeness. We can expand the comparison to Snowflake SNOW 0.00%↑ and Datatog DDOG 0.00%↑ , which I often use as comparable companies.

Datadog and Servicenow currently show best-in-class marginality among peers with a ~78% GAAP Gross Margin.

Below you can find the same chart related to the NON GAAP Gross Margins.

Palantir’s ~80% Gross Margin Adj. is second only to Servicenow.

Conclusion

Palantir is still relatively small but already shows clear signs of strength from the comparison with the most successful B2B SaaS. With the right execution, Palantir’s FCF is set to have a long way. I am excited to track and share this journey with you.

“We're going to stay small and nimble. We are hiring, but we're not like a body shop”. - Alex Karp, Palantir CEO

Yours,

Arny

View expresses are my own and do not represent Financial Advice in any way.

I own (many) PLTR stocks.