Palantir vs the Wall Street SCAM

Don't pay protection? We WACC you

Editor: Emanuele Marabella

Hi, I’m Arny. Thank you for joining 1.585 investors who receive the deepest Palantir research. Please hit the ❤️ button if you enjoy today’s article.

The fact that Palantir is not particularly appreciated by Wall Street is quite a known fact. Yet it seems there is something more than pure aversion.

Without exception, all analysts having a sell/hold rating on Palantir have a buy/hold on Snowflake and Datadog.

Thank you @em013L for the brilliant tweet.

Snowflake and Datadog are the companies Palantir is often compared to in terms of multiples, as they all belong to the “high-growth SaaS” cluster.

Is Palantir actually bullied by Wall Street? Let’s find out.

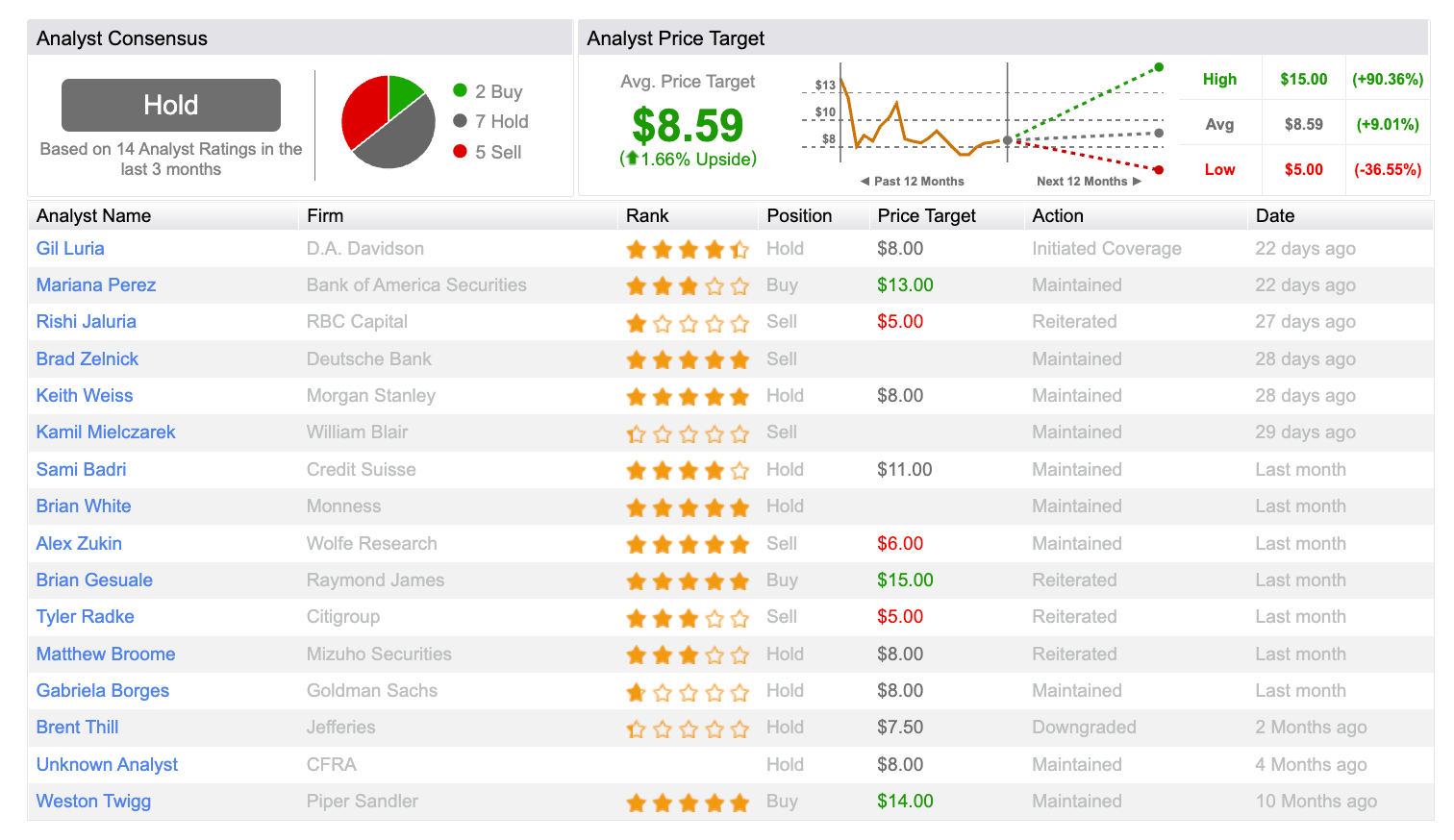

How analysts see Palantir

According to analysts, at the current price of ~$8, there is no upside left. Their average target matches the current price, in line with what we mentioned in the latest article (Palantir DCF: 20+20 is not 10+30).

In particular, in the last 3 months, Palantir received 14 recommendations of which only 2 were BUYs!:

5 SELL;

7 HOLD;

2 BUY.

The divergence in opinion is quite dramatic with Bofa, Raymond Jams and Piper Sandler hinting at $14-15 per share, while RBC, Citibank, and Wolfe Research hinting at $5-6.

How can the same company be worth 3x what another analyst say?

This should be due to a different level of understanding which lead to different assumptions for the future. As mentioned in the last article analysts have two powerful levers, or “magic numbers,” to achieve the valuation they want to fit with the narrative:

WACC;

Terminal Growth Rate.

While the usage of a 2-3% Terminal Growth Rate is quite a proxy, the choice of WACC is more prone to the analyst's opinion. Therefore, there could be large and sometimes absurd discrepancies.

As a reminder, WACC (Weighted Average Cost of Capital) is the discount rate with which future cash flows are discounted and represents a measure of the perceived riskiness of the business. The higher the WACC the less valuable future cash flows.

Bank of America and Morgan Stanley use a 13% WACC for Palantir.

Interestingly, despite using the conservative 13% WACC, Bank of America has a $15 valuation, while Morgan Stanley hints at $8 per share. This means they have a different “fair” terminal growth rate or terminal multiple.

A special thanks to @chrisj_128 for helping collect WACCs from equity reports.

Analysts on Palantir peers

What do analysts imply for the companies we usually compare Palantir with?

Snowflake: 11.3% WACC by Morgan Stanley

Servicenow: 11.4% WACC by Morgan Stanley

Datadog: 10% WACC by Jefferies; 12% by BTIG

Analysts use for Palantir a WACC which is ~2% higher than for comparable companies.

This heavily penalizes Palantir’s “fair value.”

As we showed in the latest article a “simple” 2% variation in WACC has a substantial effect when it comes to valuation.

In particular, we demonstrated that a 2% variation in WACC generates a ~28% variation in the valuation.

If you are a Palantir Bullets long-term reader you know that I consider Servicenow Palantir’s closest comparable (Seeking the Alpha: PLTR vs NOW) in terms of financial profile and business model.

I see no reason why in the next 1 to 2 years, Palantir should not be valued with 11% WACC, in line with Servicenow.

In particular, Palantir:

Achieved GAAP Profitability since the last quarter and expects to be profitable for ‘23. GAAP profitability makes Palantir even more similar to Servicenow.

Receives recurring revenues from the most prestigious companies;

Almost half of its business comes from the Government, which is considered “high-quality Revenue” since it is steady amid uncertainty.

Why is Palantir bullied? This could be related to the process of going public.

Let’s examine the Snowflake case closer.

In the following part of the article, I investigate Snowflake’s relationship with banks and how that affects their judgment. To read the remaining part of the article please consider upgrading to a paid subscription.

Snowflake pays

Snowflake went public in Q4 with Palantir. However, rather than following a Direct Listing Process, they routed toward the traditional IPO process which means charging investment banks to sell the company shares.

Snowflake’s choice of pursuing an IPO rather than a DPO is clearly a “bank-friendly” move.

In order to IPO, companies pay bankers high fees to:

perform a roadshow with its institutional clients (book building);

ensure a minimum of demand is covered (greenshoe).

Conversely, in a DPO process, the fees are minimal. I consider it the difference between purchasing a house by having a real estate agent compared to purchasing the house directly from the owner.

You can get the same result, by paying less but assuming more risk.

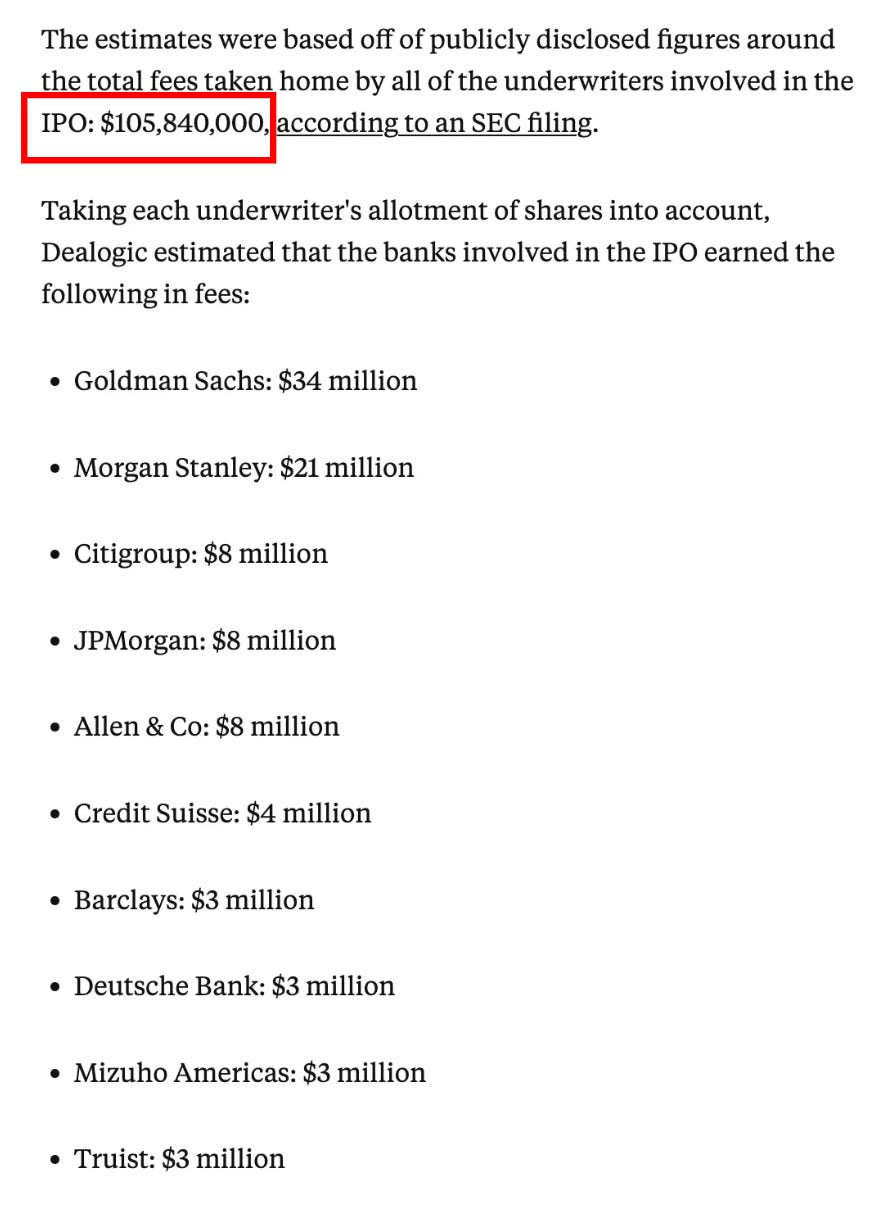

Snowflake raised $3bn in IPO at $120 by paying $106mn to ~20 investment banks, basically involving all the major investment banks.

The effect of the IPO could persist. By looking at Snowflake’s current analyst recommendations we notice:

almost half of the analysts covering the stock were involved in the IPO process;

no bank has a target price below $120;

there is only 1 sell rating among 27 recommendations in the last 3 months.

The banks paid by Snowflake to run the IPO process have a target price that is ~13% higher than the already generous $172 /share target price (+35% upside) from banks that didn’t participate in the IPO.

Coincidence?

One could argue that after a ~70% drop from the peak, Snowflake’s price has become incredibly appealing. Is this the case?

At $190, which is the average target price by analysts, Snowflake’s valuation would imply:

13x EV/Sales on 2028 $9.7bn Sales;

70x EV/EBITDA on 2028 $1.7bn EBITDA;

These numbers clearly do not indicate a “cheap” company for a growth that, according to their guidance should decrease to ~30% by 2028-2029.

Furthermore, if we calculate the implicit assumptions, we notice analysts use:

11% WACC despite Snowflake not being GAAP profitable;

8.6% Terminal Growth implied by using a 70x EV/EBITDA Terminal Value.

For whoever has worked with professional valuations, a ~9% Terminal Growth Rate should only scream one word: scam.

In my experience as an analyst, I would argue that whatever number is higher than 3-4% is misleading as the terminal growth rate should gravitate toward the GDP growth.

A terminal growth rate of 9% implies that Snowflake would grow in perpetuity at a much faster rate than the world GDP .

Clearly a stretched assumption.

To be clear, this doesn’t mean that Snowflake can’t rise further, but the implied expectations are already so high that the margin of safety is little. Any mistake in execution will be heavily penalized.

Snowflake, paying substantial fees for the IPO, seems to have brought the sympathy of Wall Street.

Palantir on the other hand started quite adversarial with Wall Street by going through the DPO process and the affirmations of Karp calling the financial industry “the malicious forces of banking.” these 2 years have not helped obtain favor with Wall Street.

Conclusion

The fact that Wall Street is quite adversarial to Palantir is no surprise. I consider this actually a positive sign hinting that we are at a price that incorporates many adverse factors:

the slowdown is assumed to be permanent;

the misconception that Palantir is not a software company despite 80% gross margins;

banks taking “revenge” for not having followed the traditional “IPO route.”

Since Servicenow and Snowflake are valued at 11% WACC, I don’t see why Palantir over time should not be valued based on the same assumption over time.

If Palantir keeps performing, the narrative will take care of itself, no matter what analysts think. Over time, the company with the best business wins.

“As for the stock market, at times it likes us, at other times not. Long-term evolution is rational, not year-on-year.” - Alex Karp, Palantir CEO, L'Obs interview

Yours,

Arny

Love this article! Well done 👏🏼

let it snow let it snow let it snow ;)) ... until it gets melted ;))