Palantir: the QoQ Decline

Bug or feature?

Editor: Emanuele’s Notepad

Hi, I’m Arny 😊 Join more than 740+ fellow Palantir investors spotting asymmetries with the subscribe button below. Research articles are free. You could support my work with a paid sub.

In the Q3 analysis article, we assessed that the decline in YoY growth of the Palantir Commercial business was mainly due to the “SPAC distortion” (Palantir Q3: Another “Disaster”?).

However, we also saw a -1.5% QoQ decline in non-SPAC Commercial Revenues from $179mn in 22Q2 to $176mn in 22Q3.

Should we be concerned about this decline?

Palantir as a “Consultancy”

The QoQ decline could be attributed to Palantir’s relatively high incidence of Professional Services compared to other software companies like ServiceNow and Salesforce. Thank you @OnlyCFO for pointing me in this direction.

Professional Services are on-demand consultancy projects.

Palantir describes its Professional Services as customer support, mainly driven by configuration and training. More specifically:

Our professional services support the customers’ use of the software and include, as needed, on-demand user support, user-interface configuration, training, and ongoing ontology and data modelling support. Professional services are on-demand, whereby we perform services throughout the contract period; therefore, the revenue is recognized over the contractual term. - Palantir 10k

Unfortunately, we don’t know Palantir’s breakdown between pure Software Revenues and Professional Services.

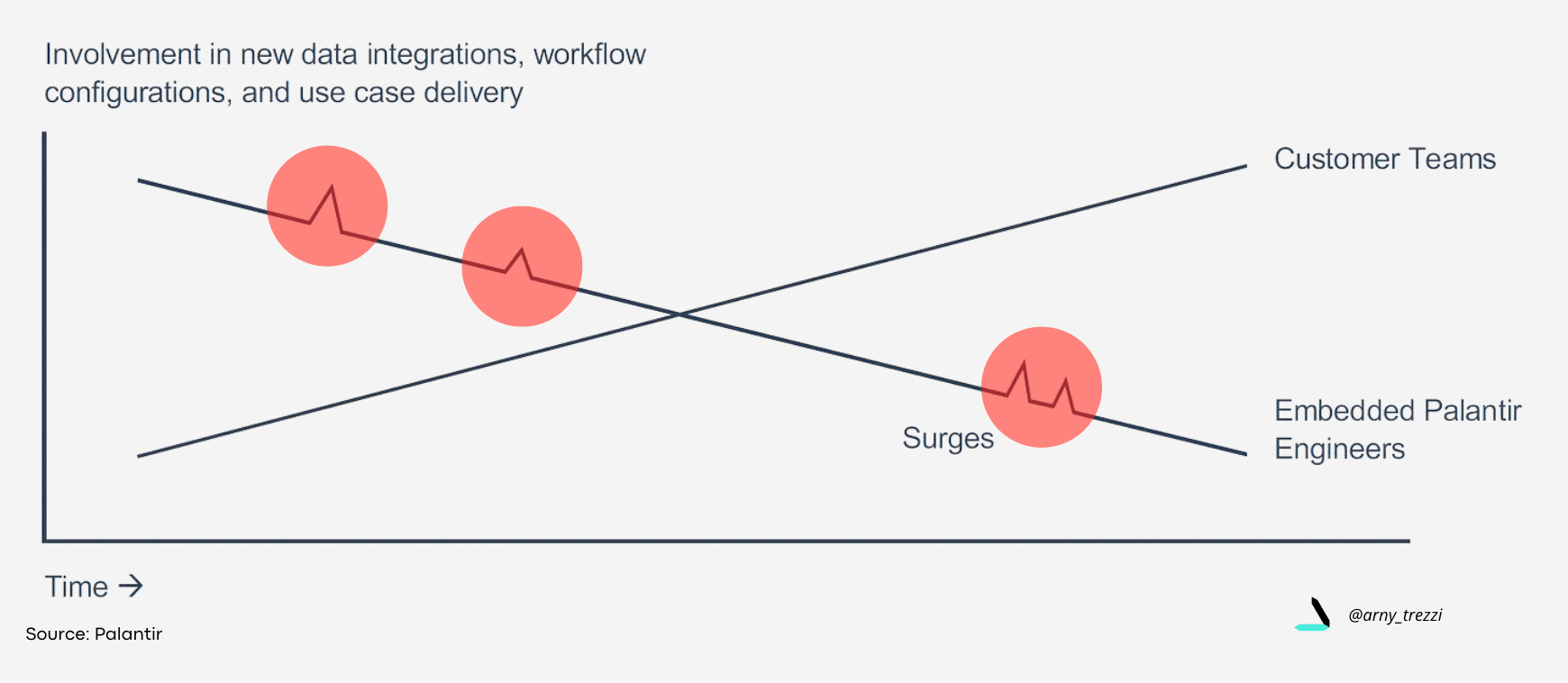

We just know that Foward Deployment Engineers are working closely with customers as “consultants” in order to solve their problems. This is Palantir’s secret source to generate strong relationships and set the basis for a prolonged and expanding usage of its pure software solutions.

The embedded Palantir engineers working with a client, decline over time as the customer scales, but could spike due to major implementations.

The “on-demand” nature of these consultancy projects makes them particularly vulnerable to macroeconomic volatility. When CEOs are not confident in the economic outlook, they cut back on high discretionary spendings like Advertising and Consultancy.

We could synthesize:

On-demand = discretionary spending = sensitivity to macroeconomic changes;

Subscription = “pay no matter what” = resiliency to macroeconomic changes.

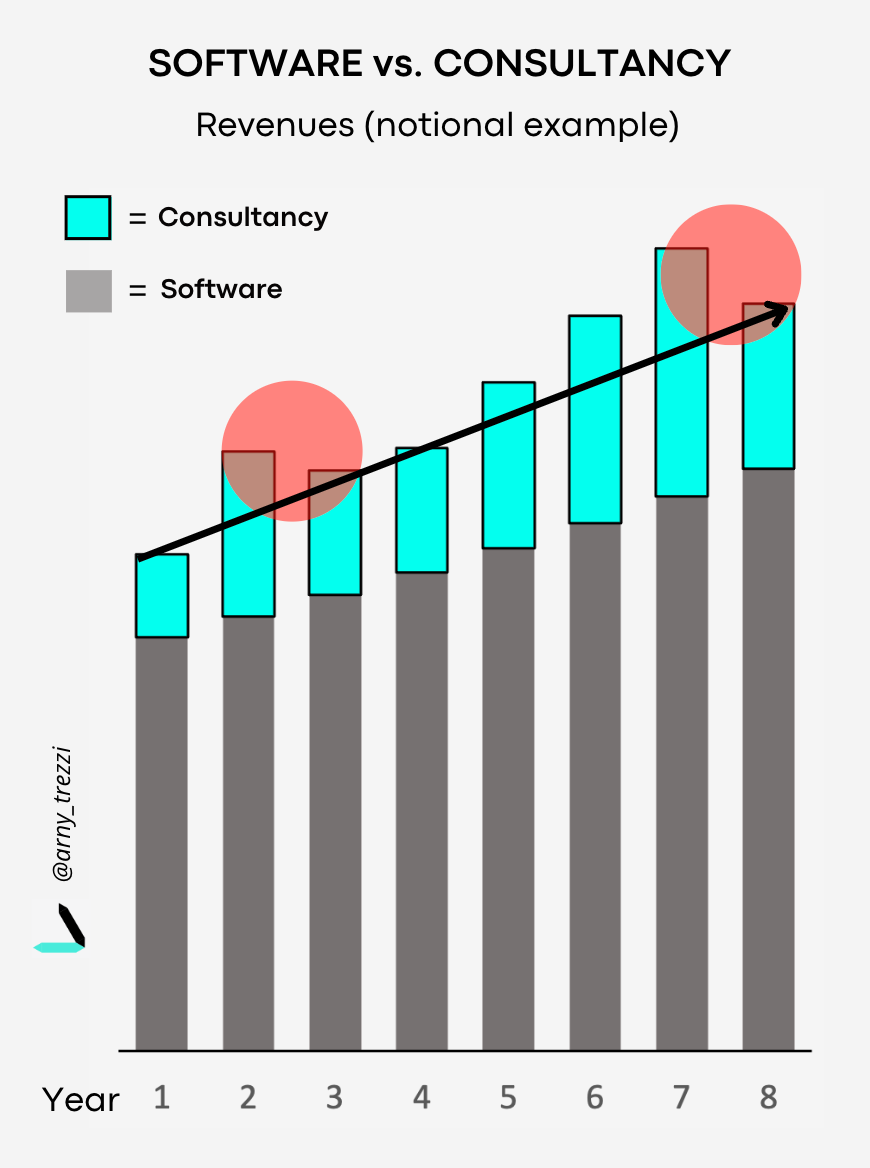

In a hybrid mix like Palantir, the spikes and the following declines could be stronger than the other B2B companies, which rely more on subscriptions. Clearly, Palantir seeks to increase the component of software as it scales because that offers higher margins and scalability.

You can see visually with the example below how a consultancy could create “bumps” in the overall Revenues, while Subscriptions grow steadily every quarter.

As shown previously, CEOs’ confidence is now at historic lows, affecting the level of Professional Services needed.

Therefore, the Commercial QoQ decline could have been driven by a drop in Professional Services, which conversely, were strong in Q2.

Peers check

Supporting the fact that the QoQ decline was mainly driven by reduced on-demand projects, we can see the results of two comparable businesses:

NOW 0.00%↑ Professional Services Revenues ( ~5% of Revenues) declined ~5% QoQ;

Accenture’s (biggest IT Consultancy company) Revenues declined ~5% QoQ.

The comparison with ServiceNow and Accenture supports the idea that Palantir’s QoQ decline was driven by lower on-demand projects due to macroeconomic uncertainty rather than a structural problem in the business.

Accounting adjustments

Another possible cause that could have affected the quarterly numbers could be an accounting adjustment, similar to what happened in Q1 with SPACs.

In Q1, SPACs generated an anomalous $39mn in Revenues after $26mn in Q4. During the Q1 earnings call, this was explained as an accounting “catch-up”:

“Going forward, expect about $30 million of revenue per quarter from these customers. Revenue in Q1 is higher as a result of some catch-up of about $9 million recognized in the quarter, reflecting work we started last year.” - Kevin Kawasaki, Palantir Head of Business Development.

Conclusion

Some volatility in quarterly numbers is normal, despite not being pleasant to the eyes of shareholders. On the other hand, if a negative trend emerges, then that would be a serious problem that could underpin the health of the business.

Unless we start seeing a structural decline that breaks the positive trend, I don’t see a reason to worry.

Yours,

Arny

Join me on:

Twitter: @arny_trezzi

Youtube: @Arny Investing

Instagram: @arnylaorca

Join Emanuele20x on:

Twitter: @Emanuele20x

YouTube: @Emanuele20x

Substack: Emanuele’s Notepad

View expresses are my own and do not represent Financial Advice in any way.

I own (many) PLTR -1.34%↓ stocks.

Great article, Arny!

bravo Ema bravo Arny, thank you & kudos!