Palantir Q3 - What I'm looking for

Q3 earnings are near! Here are the most crucial drivers.

Editor: @Emanuele20x

Hi, I’m Arny 😊 Join more than 580+ fellow Palantir investors spotting asymmetries with the subscribe button below. Research articles are free.

Palantir just announced that it is going to release its Q3 results on November 7th, 2022.

This quarter could be a “make it or break it” moment for its business and stock price. We better get an idea of what to expect.

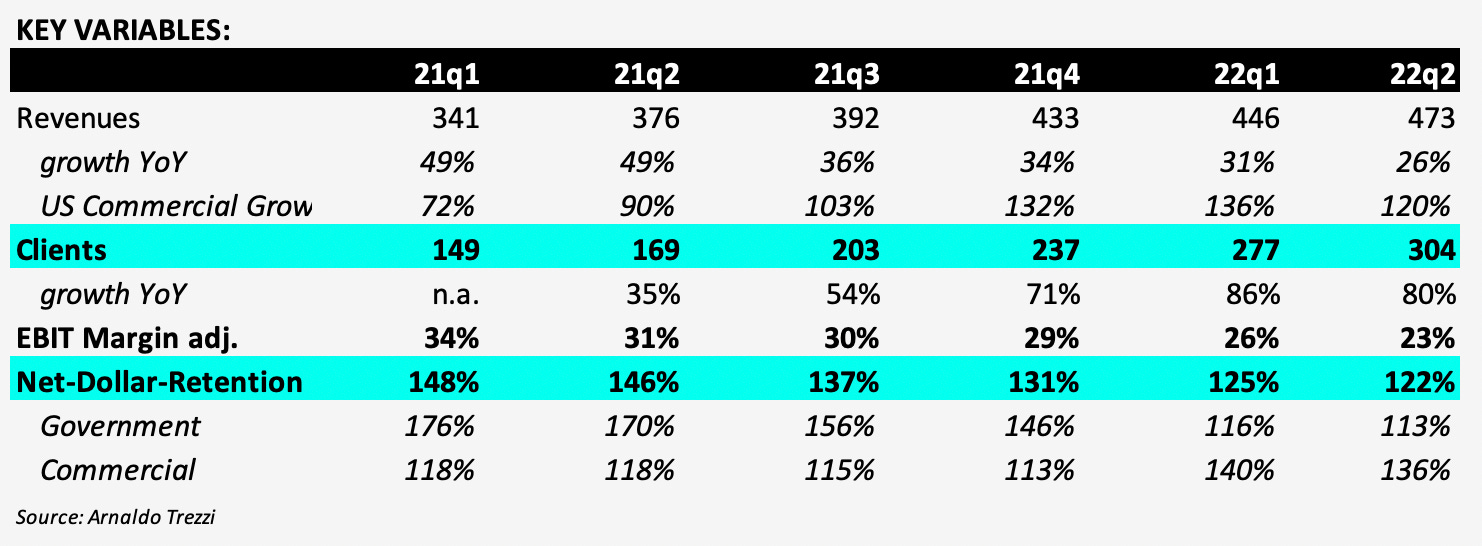

Concerning Q3 results, I will pay particular attention to the same key metrics that I underlined before the Q2 results (Palantir Q2 - What I am looking for):

Client growth: it would be great to see more than 40 new additions. The Commercial business should benefit from positive seasonality (PLTR Q1: better than it seems) as most companies plan their budgets in Q3-Q4;

Net Dollar Retention: it is crucial to stay above 120%, especially in the Commercial Sector. This is the most important metric which tracks the growth durability (PLTR in 2032: A Jump in the Future);

US Comm. Revenue growth: I seek continued growth above +100%, combined with strong client acquisition. Again, this is the most important segment to track because it is the key driver for Palantir’s growth (PLTR US Commercial is the Key).

The headwinds that affected Q2 results have continued to persist:

Government was mainly affected by delays to the Department of Defense (DoD) budgets (PTLR Government Slowdown: Not Palantir’s Fault Only);

Commercial was negatively impacted by Forex (Is Palantir Commercial Doomed? Pt.1) and recession fears that caused longer sales cycles (Is Palantir Commercial Doomed? Pt.2). These headwinds are strong in Europe; therefore, I believe US Commercial could acquire many more clients than International (PLTR US Commercial is Taking the Lead).

I don’t expect groundbreaking results from this quarter, which already received reduced Guidance with $475mn Revenue. This would consist of ~21% YoY growth, well below the long-term Guidance of ~30%.

However, I do see a high probability of a Guidance Revision for Q4, driven by the strong contractual activity from the Government side and positive clues from activated links on the Commercial side.

Crucial progress

There are hints that Palantir’s contractual activity is progressing well:

The recent contract rain from the US Government (PLTR Government: It’s Raining) shows that Palantir is capturing the unique opportunity window it has (PLTR Government: It’s Now or Never). @Palantrillion shared detailed calculations hinting that the new awards should generate a supplemental ~$80mn per quarter on the Government Side. These should support a Guidance Revision, which apparently was weak due to the uncertainty of major contracts. These contracts were signed after the Q2 release.

IL-6 Accreditation. Palantir has been awarded IL-6, which is the highest standard of SaaS security clearance for the DoD. Only Palantir, AWS, and Microsoft Azure are authorized to work with this level of security, which is considered “Top Secret.” Thanks to this achievement, Palantir could be selected as a provider for huge new potential contracts, such as the $9bn Warfight Cloud Capacity (JWCC) project.

This news confirms what we discovered back in April. This achievement is another hint that the Government side is in good shape and suffered from a non-problematic slowdown (PTLR Government Slowdown: Not Palantir’s Fault Only).

Strong “new active links” have been generated on the Commercial side. @Either_Square just published the Dossier 4.0 which shows that during Q3, 132 new active links have emerged. From the previous Dossier 3.0, released on April 22nd 2022, new 229 entities were revealed. We can consider an active link as a hint that a potential client is at least in the pilot phase. As a reminder, not all pilots will lead to a contract, therefore only links which are active for more than ~6 months should be considered “clients.” Despite this limitation, active links could be considered an alternative leading indicator of commercial activity.

Among the clients/partners acquired, there are some really important names like Tier 1 consultancies (McKinsey, BCG) and industry leaders like Gilead and Philips 66.

Regardless of the weaker than expected Q2 results, the development above suggests that the operating machine is trending in a positive direction. If true, long-term results and stock price will follow.

A further hint comes from Alex Karp’s most recent interview where he exuberated confidence in the US business (61% of Revenues):

“We’re seeing pretty significant uptick in demand in the US for both Commercial and Government” - Alex Karp, Palantir CEO.

Yours,

Arny

Join me on:

Twitter: @arny_trezzi

YouTube: @Arny Investing

Instagram: @arnylaorca

Business Email: arnylaorca@gmail.com

Discord Channel

Join Emanuele20x on:

Twitter: @Emanuele20x

YouTube: @Emanuele20x

Substack: Emanuele’s Notepad

View expresses are my own and do not represent Financial Advice in any way.

I own (many) PLTR 0.00%↑ stocks.