Palantir costs less than Coca-Cola

This non Coke-for-Coke comparison is a provocation against "Palantir is overvalued"

Editor: @Emanuele20x

This article is a provocation for those who think “Palantir is overvalued” without really digging into the financials.

The “ugly truth” is that Palantir now trades at a lower valuation than Coca Cola.

From the chart below we can see how Palantir's valuation on ‘22 numbers relates to that of Coca-Cola, a couple of B2B SaaS peers and major Consumer Brands.

This is not a Coke-for-Coke comparison. Coca-Cola is the benchmark of steady cash cow operating Retail with a long history of dividends. Palantir’s business and its financial history are very different, but I believe the comparison could help us better understand how Palantir is perceived by Wall Street.

We observe:

Palantir: 25x EV/FCF vs 20% FCF Growth expected;

Coca-Cola: 27x EV/FCF vs 1% FCF Growth, virtually no growth expected.

Palantir is cheaper than Coca Cola despite much higher growth expected.

Palantir’s 20% growth is conservative because it includes the “strong” 10% to 6% dilution by ‘24 assumptions (mentioned in my previous article). Without further dilution, FCF per share could grow +30%, in line with the guided Revenues.

As mentioned previously, EV/FCF is the best measure to compare any investment, so even very different companies like Palantir and Coca-Cola, because it reflects the value of the “cash flows to the business owner”.

In particular, EV/FCF is more accurate than PE for the following reasons:

It includes Debt into the valuation, which “increases the cost” for the potential buyer of the business.

FCF is more indicative for SaaS companies than PE due to high SBC, which affects earnings, but doesn’t impact FCF.

Why should Palantir's valuation be lower than Coca Cola?

From a financial theory standpoint, this occurs for 2 main reasons. Both reasons are associated with interest rates:

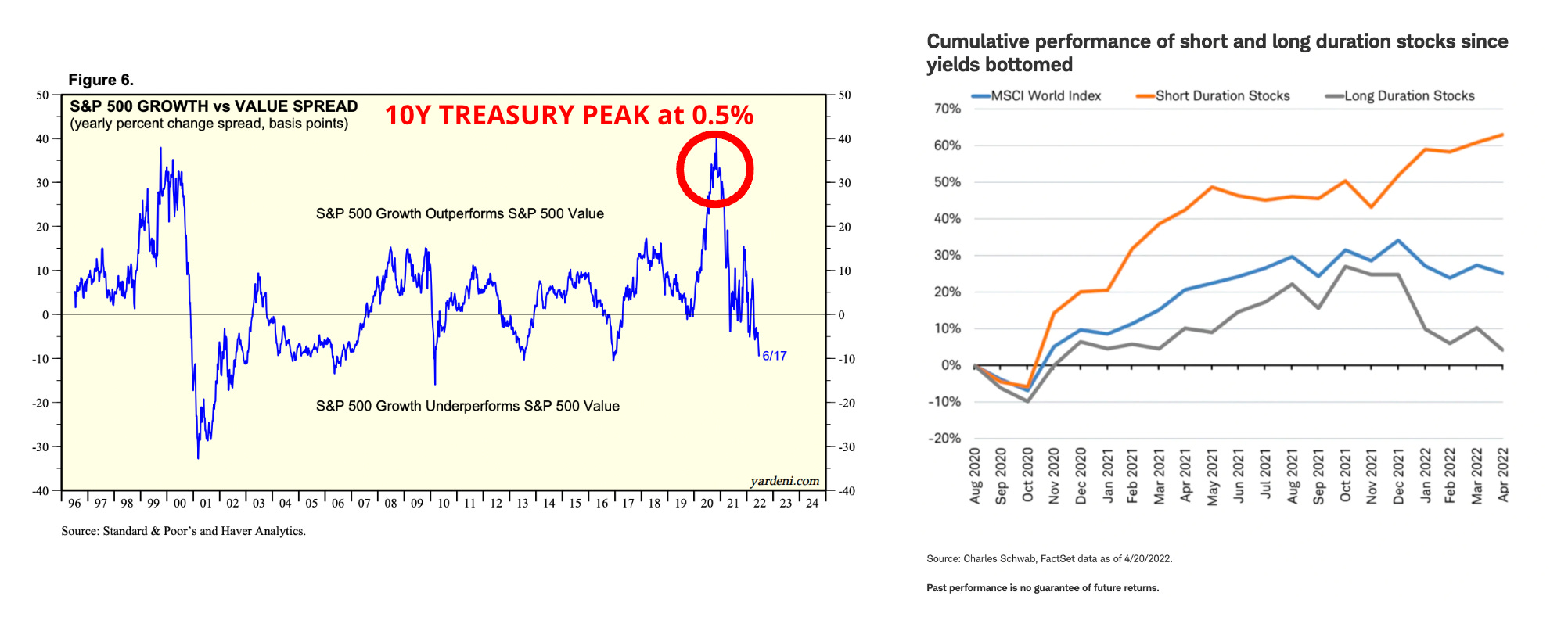

1. Inflation benefits “value stocks” and penalises “growth stocks”

The professional portfolio managers framework works as follows:

Low interest rates = good for “growth”.

High Interest rates = good for “value”.

The idea is that high inflation is associated with higher interest rates and high-interest rates make the future cash flows less attractive.

According to financial theory, so-called “Growth companies” like Palantir see a large component of their earnings in the future. This leads to more sensitivity to high-interest rates (they drop more as interest rates raise), therefore these companies are called “long-duration assets”.

On the other hand, more mature “Value stocks” like Coca-Cola are considered “short-duration assets” and “safer” during inflation. Steady cash flows often paid out as dividends, attract many investors which are willing to pay a premium for the perceived “safety”.

A take from InstitutionalInvestor:

“As inflation soars, value stocks around the world offer a safe haven for investors, [thanks to] their outstanding forecasted long-term real returns,” Brightman concluded.

We could summarize:

Growth stocks = long duration = fall much if interest rate raise = “risky”;

Value stocks = short duration = fall little if interest rate taise = “safe”.

In this environment of high inflation, investors prefer companies that produce steady cash flows now. On the other end, they pay little for companies having strong growth prospects in the future.

This, according to financial theory explains why Palantir and Coca-Cola trade at similar multiples despite the growth profiles being very different.

However, the “growth vs value” considerations are extremely flawed because they relate to stock movements and do not really consider how certain businesses perform in a determined environment. Theory fails to capture the idea that during inflation EPS growth is the only thing that makes investors better off.

If inflation is at 8%, you need 8% FCF growth just to break even.

As a result of the flawed narrative, companies with the “growth label”, strong cashflows generation and cash balances, like Palantir, are unfairly penalized.

This leaves space for an asymmetrical opportunity.

2. Coca-Cola has a Lower Cost of Capital

This section is more financially technical. Here is the bottom line:

Palantir is perceived as “risky,” therefore its cash flows are worth much less than those coming from a “safe” company like Coca-Cola.

For the technically savvy, the Weighted Average Cost of Capital (WACC) is the rate used in financial models (DCFs) to discount future cash flows. This reflects the idea that future cash flows are less valuable than present ones.

WACC = (% of Equity)*Cost of Equity + (% of Debt) *Cost of Debt*(1-tax rate).

The higher the WACC, the less valuable the future cash flows. Conversely, the lower the WACC the more value is given to future cash flows.

As a reminder:

Cost of Equity = Risk-Free Rate + Beta * (Market Return - Risk Free)

As you can see the Cost of Equity is highly influenced by:

Risk-Free Rate (generally the 10y Treasury): when interest rates rise, all financial valuations are affected negatively.

Beta: measures the sensitivity of the stock to the market under the hypothesis that the risk of the business is reflected in the volatility of the stock. Remember: in financial theory “Volatility = Risk”.

Coca-Cola WACC is low, around 6-7%, for 2 reasons:

0.8x Beta, which is considered “low”. This means Coca-Cola stock has relatively little sensitivity from variations in the S&P500, which has 1x Beta. This translates into a lower cost of equity which in turn supports the valuation.

Debt, which decreases the WACC. For a company, there is a smaller cost in issuing Debt than Equity. As a proxy, you can consider the Cost of Debt generally is around 3-5% (depending on the Credit Rating), while the Cost of Equity generally stands between 7-10% (depending on the Beta). In the case of Coca-Cola, the debt costs 3-4%. In addition, Debt generates a tax shield effect which contributes further to reducing the WACC since Interest Expenses are tax-deductible. Therefore the presence of “good debt” helps lower the WACC, which in turn increases the financial valuation.

Investors know that Coca-Cola is an incredibly stable business, which can survive and pay dividends in difficult times, therefore they are happy to “pay a premium for safety”.

On the other hand, Palantir's Cost of Capital is relatively high at ~10%, coming from the combination of:

1.5x Beta, which is considered “high” to reflect the substantial volatility;

No Debt, which means only the Cost of Equity is included in the WACC.

These parameters greatly impact the financial valuation because DCF models are highly sensitive to a small change in WACC assumptions.

A simple 3% difference in WACC could generate an almost 2x “Fair price”.

In particular, we can observe how much the fair valuation would change in our sample DCF by changing the WACC:

7% = $27 per share;

10% = $15 per share;

15% = $8 per share.

WACC is only based on market factors. Therefore, when the WACC is high, but the business, in reality, is “safe” a discrepancy emerges. This could be an opportunity.

Conclusion

From the standpoint of the financial theory, Palantir deserves a similar or even lower multiple than Coca-Cola despite the much higher growth.

This would make sense if we lived in the textbook world. However, by looking at the full picture, from a business owner's perspective, things could appear much different.

If we assess Palantir, in reality, as much safer than the market perceives and we pay a low price for the growth prospects, our margin of safety could increase exponentially.

“The three most important words in investing are margin of safety.”- Warren Buffett

I am looking forward to debunking financial myths more in detail with you. Subscribe to discover them together!

Arny

Join me on:

Twitter: @arny_trezzi

Youtube: @Arny Investing

Discord Channel

View expresses are my own. Do not represent Financial Advice.

I own (many) PLTR 0.00%↑ stocks.

Disclaimer: Coca-Cola is an extraordinary business. I take it as an example to show that considerations like “Palantir overvalued” without the full picture could lead to very wrong conclusions.

| A guest post by

|

By the time the market decides to embrace it, we will be so ahead of the game.

And Yes, the sentence brings you back to the core of Palantir. It’s not a matter of why you need it but how to use and apply it.

Arny, I loved the comparison. I actually just tweeted this:

Palantir will continue to benefit from accelerated US commercial adoption as customer counts and average pricing per customer metrics show sharp improvement.

As $PLTR CEO stated:

“The quality of the questions has shifted from why would we need this to how would I use it?”