Is Palantir Recession Proof?

With the upcoming fears in the global economic scene, there is reason to believe that Palantir will continue to not only grow but possibly thrive during these uncertain times.

Editor: @Emanuele20x

Can Palantir Survive a Recession?

Clues come from the history of comparable companies during the Great Financial Crisis.

By assessing these comparables we can obtain a better understanding of the negative impact on Palantir’s business if a major recession happens.

Short answer: none.

B2B Recurring businesses are incredibly resilient to downturns

Companies providing “existential” products remain profitable even during economic downturns.

IT Software is as existential for companies as food or medicines for humans.

While in a period of strong economic contraction many companies suffered major reductions in earnings, IT Software showed the same resilience as HealthCare and Consumer Stables.

You cannot operate a company without software.

Similar to electricity, the cost structure depends on the total usage but its necessity cannot be omitted.

Some clients can delay payments while others can default, but the Recurring Revenue and the diversified mix of sectors of the client base help protect against these occurrences.

Clues from Salesforce’s and ServiceNow’s past

As mentioned previously, I consider Salesforce and ServiceNow the two closest comparables to Palantir as successful B2B Cloud businesses.

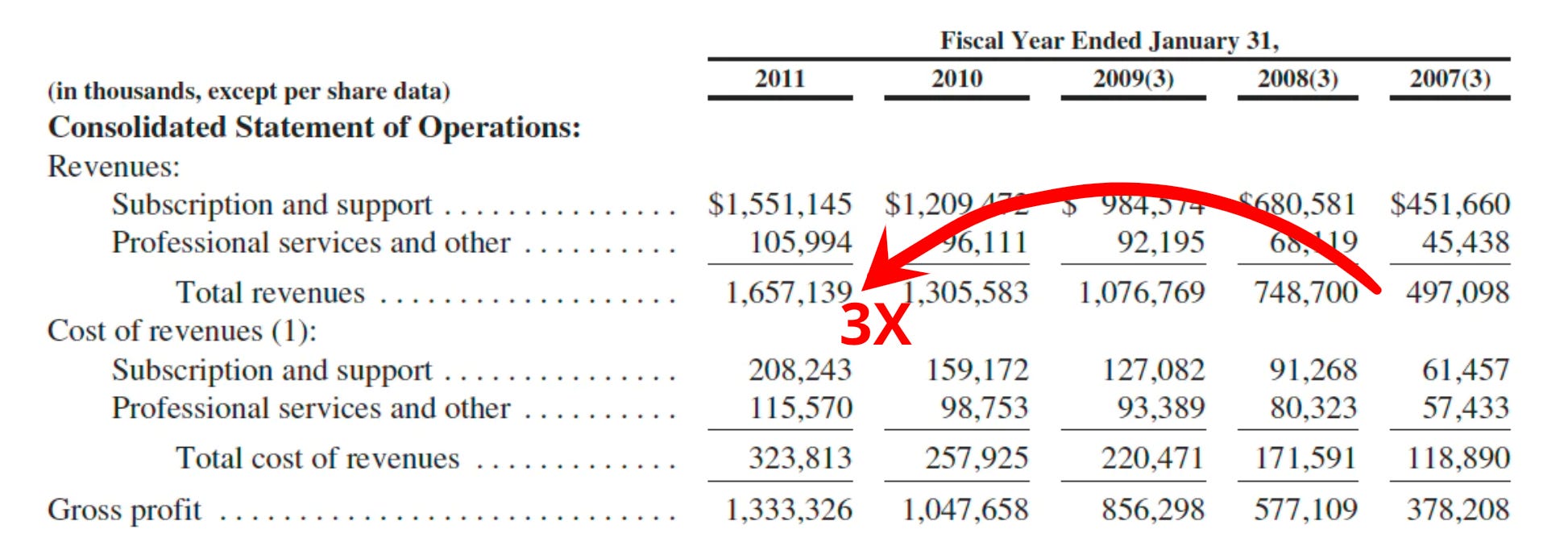

Salesforce

Salesforce's Revenues tripled in 4 years during the economic contraction:

+50% in ‘08;

+44% in ‘09;

+22% in ‘10;

+28% in ‘11.

ServiceNow

ServiceNow, born in 2003, grew its Revenues more than 50x during the ‘07-‘11 period reaching almost $80mn:

+377% in ‘08;

+109% in ‘09;

+122% in ‘10;

+97% in ‘11.

Clearly, ServiceNow numbers started from a small base but its growth trajectory has been stunning.

Clues from CEOs

Recent interviews of ServiceNow’s and Salesforce’s CEOs highlight the strength of the B2B businesses during downturns.

“We are in a Sustained demand environment for Enterprise software. Our customers need us more than ever”.

“If we slow investment in the short lose ground in the mid term and we go out of business in the long term.”

“You will see Enterprise customers invest in business software to deal with all the challenges: inflation, supply chain, dislocations, war in ukraine.

“They are not buying software, they are buying business outcomes”.

Salesforce co-CEO expressed similar thoughts:

“Digital technology is more relevant in a downturn than it is in an upturn”.

We could synthesize great B2B SaaS are crucial during downturns because their products allow clients to generate new business and save costs.

Software is the only way out.

The importance of Software is highlighted by a recent Chief Information Officers survey by JP Morgan. Snowflake, Microsoft, ServiceNow, and Salesforce are among the companies in which clients will increase spending despite the current fears of a coming recession. Palantir was not included in the survey, probably because of their small client base.

Market offer opportunities during downturns

During 2008 Salesforce crashed by more than 70% in 3 months. This crash happened despite the incredible revenue growth which occurred during this period as previously stated.

The crash was not due to overvaluation before the crash. It was trading close to 8x EV/Sales.

The crash happened because the aggregate index received a major hit. As mentioned in the previous article, Tech is considered a “Risky Sector”, so it is generally sold during downturns.

Therefore, Salesforce in 2008 offered a great asymmetry:

business striving during a crisis;

stock price decimated.

For the Salesforce shareholders, spectacular returns happened thereafter as the company kept growing +20% up to now.

The stock increased +3000% since 2008 despite the recent 40% drop!

Palantir’s opportunity

Palantir has been hammered by the inflation narrative combined with recession fears.

I believe Palantir is in a similar situation to Salesforce during 2008:

Recurring Revenues benefitting from Supply Chain issues and global conflicts;

Attractive valuation, trading at a similar EV/FCF as Coca-Cola.

This, in my opinion, is a precious asymmetry that an investor can capitalize on.

We will have precious hints of the size of the asymmetry in the upcoming Q2 results.

Yours,

Arny

Join me on:

Twitter: @arny_trezzi

Youtube: @Arny Investing

Discord Channel

View expresses are my own. Do not represent Financial Advice.

I own (many) PLTR 0.00%↑ stocks.

Wonderful piece!

Masterclass, arny sees where the puck is going, this should be the narrative for pltr for the next 24 -36 months…