Fight! PLTR US Commercial vs SNOW

How much is Palantir US Commercial worth?

Editor: @Emanuele20x

Snowflake ( SNOW 0.00%↑ ) is one of the fastest growing companies in the Cloud space, therefore is often compared with Palantir.

Currently, their products and go-to-market strategies differ significantly, however, these two companies will probably converge in the future.

Similar to the comparison we made with ServiceNow (Seeking The Alpha: PLTR vs. NOW), comparing the two could provide some hints on the relative weaknesses and/or strengths of Palantir’s business.

Palantir US Comm. vs SNOW

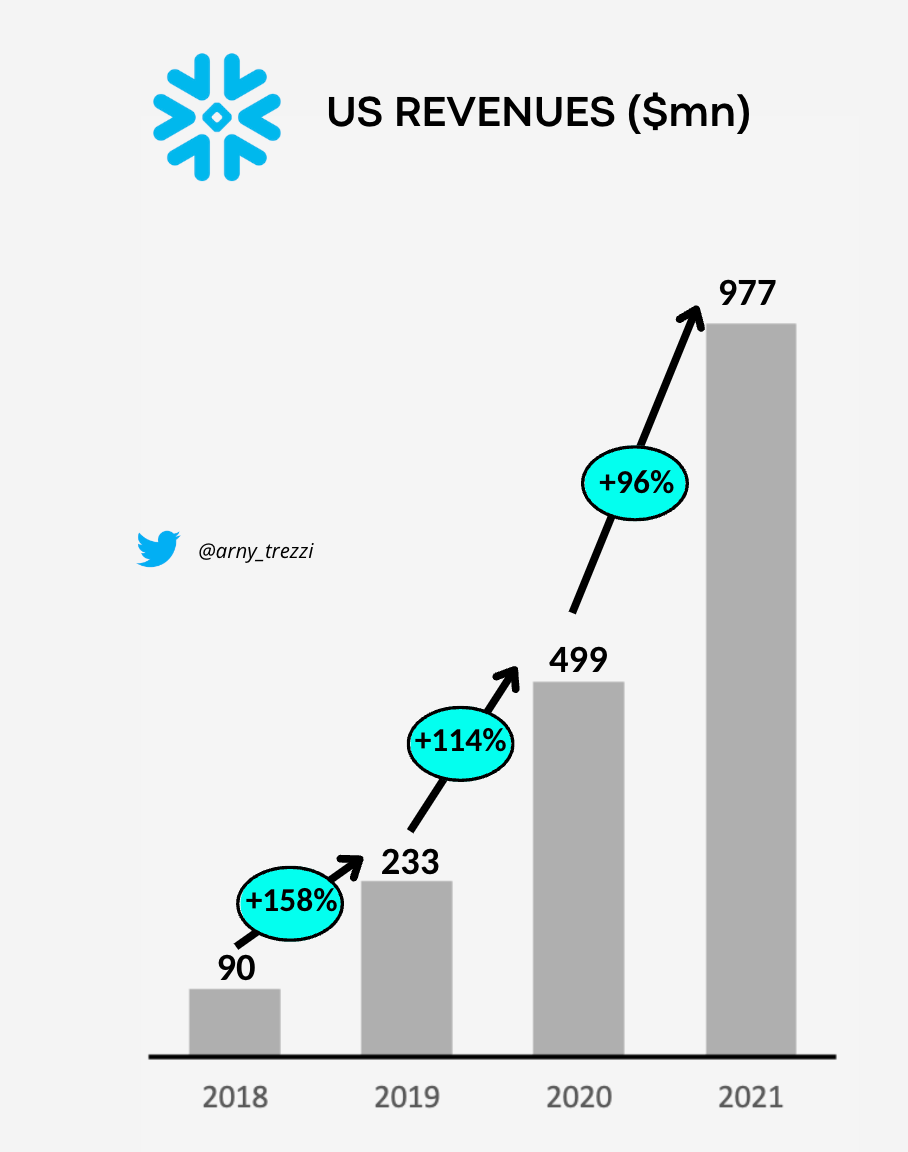

Snowflake is one of the best hypergrowth companies. As mentioned previously (Is PLTR Commercial Doomed? [part 1]), ~80% of Snowflake’s business comes from the US. For the sake of comparison with Palantir’s US Commercial, we will focus only on Snowflake’s US segment.

Snowflake US ramped its Revenues at a spectacular pace, moving from $90mn as of 2018 to nearly $1bn in 2021. That’s a whopping +121% CAGR!

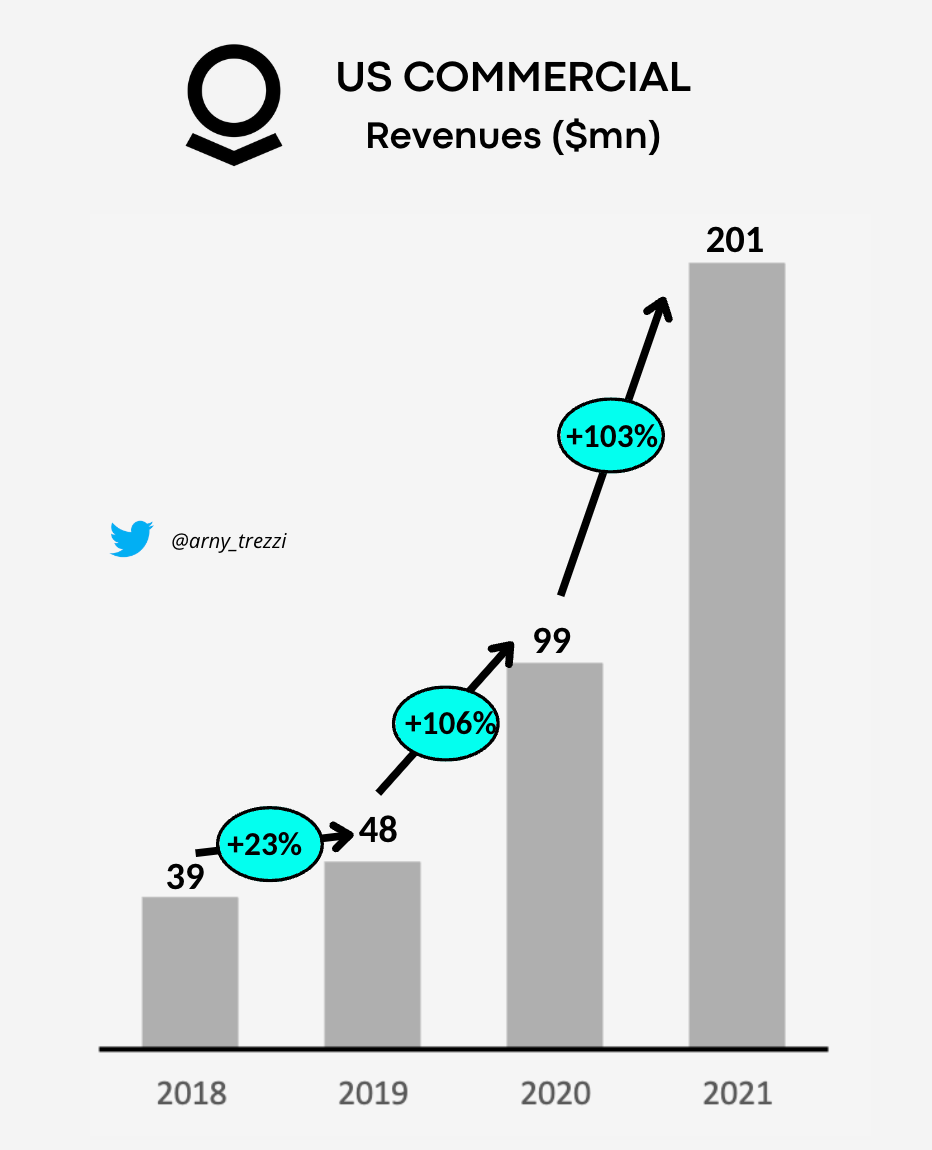

Palantir US Commercial is relatively much smaller but shows a similar growth potential at a ~$200mn run rate.

Despite a slower start, the 2020 growth really ramped up thanks to the new salesforce. Previously, Palantir US Commercial only counted on 6 salespeople, yes, SIX!

Diverging trends

By directly comparing the two growth trends we notice an interesting divergence.

Snowflake US growth rates are decreasing from +158% as of 2019 to +87% as of 22Q2.

Palantir US Commercial growth is accelerating from +23% as of 2019 to +123% as of 22Q2.

While Snowflake is decelerating, Palantir is accelerating.

I attribute the divergence to:

Size: it is harder to grow fast at scale. Currently, Snowflake US is 5x Palantir’s US Commercial.

Network Effects: Palantir has much stronger network effects (PLTR: The Biggest Networks Start Small). This means that the more Palantir grows, the more the network feedback loop helps it grow with decreasing marginal effort and cost.

To really prove how network effects matter, it will be very interesting to keep track of the chart in the following quarters.

Notably, despite the strong hiring (Palantir: Hunting Season is Open), Palantir still has a relatively tiny sales force. While sales representatives consist of ~33% of Snowflakes’s employees, they represent ~4% of Palantir (PLTR: SELL SELL SELL).

If network effects really kick in, Palantir could:

keep increasing growth while growing in size;

need relatively little sales force to sustain that growth.

How much is Palantir US Commercial worth?

Since we assessed that the growth rate of Palantir US Commercial is comparable to Snowflake’s, we could use SNOW 0.00%↑ valuation to have a hint at how much Palantir's US Commercial business could be if it was a standalone business.

Snowflake, trading at 20x EV/Sales has the richest valuation in the cloud sector thanks to its staggering growth.

Despite 20x EV/Sales clearly being a high multiple, it is in its lowest range since the IPO.

By applying a 20x Sales multiple, we could obtain a $5bn “fair” valuation for Palantir US Commercial if it traded as a standalone business.

Palantir currently trades at ~$17bn Market Cap while having more than ~$2bn Net Cash. This means the Enterprise Value is ~$15bn.

US Commercial, being worth already 1/3 of the Group, is the hidden gem.

Conclusion

Palantir US Commercial still has lots to prove and these simple considerations help us realize that there is a gem inside the group.

If the US Commercial could keep its growth, not only could it drive the Palantir Revenues as we mentioned (PLTR US Commercial is Taking The Lead), but also its valuation well above the current ~7x EV/Sales.

Yours,

Arny

Join me on:

Twitter: @arny_trezzi

Youtube: @Arny Investing

Instagram: @arnylaorca

Business Email: arnylaorca@gmail.com

Discord Channel

View expresses are my own. Do not represent Financial Advice.

I own (many) PLTR 0.00%↑ stocks.

Beautiful charts!

great take, thanks guys!